info@protectwiththeo.com

Sunday Closed

Multi-State Offices

Home / Medicare Plans

When exploring your Medicare options, plans typically fall into three categories: Medicare Supplement (Medigap) Plans, Medicare Advantage (Part C) Plans, and Medicare Part D Prescription Drug Plans. Each type offers different levels of coverage, flexibility, and cost.

Medigap Plans offer standardized benefits in most states—meaning that Plan G, for example, provides the same core coverage regardless of the insurance company you choose. However, some carriers may offer added perks such as gym memberships or discount programs for vision, dental, or wellness services. While it might be tempting to choose the lowest-cost option, the right plan isn’t always the cheapest upfront. Some carriers manage their plans better over time, resulting in smaller rate increases year after year. We can help you compare and identify which companies offer the best long-term value based on your needs and budget.

Medicare Advantage Plans are Medicare-approved health plans offered by private insurance companies and serve as an alternative to Original Medicare. These plans combine your Medicare Part A (hospital) and Part B (medical) coverage—and often include Part D (prescription drug coverage)—into one convenient plan. Unlike Medigap, Medicare Advantage Plans can vary widely in terms of benefits, provider networks, and out-of-pocket costs depending on the insurer and where you live.

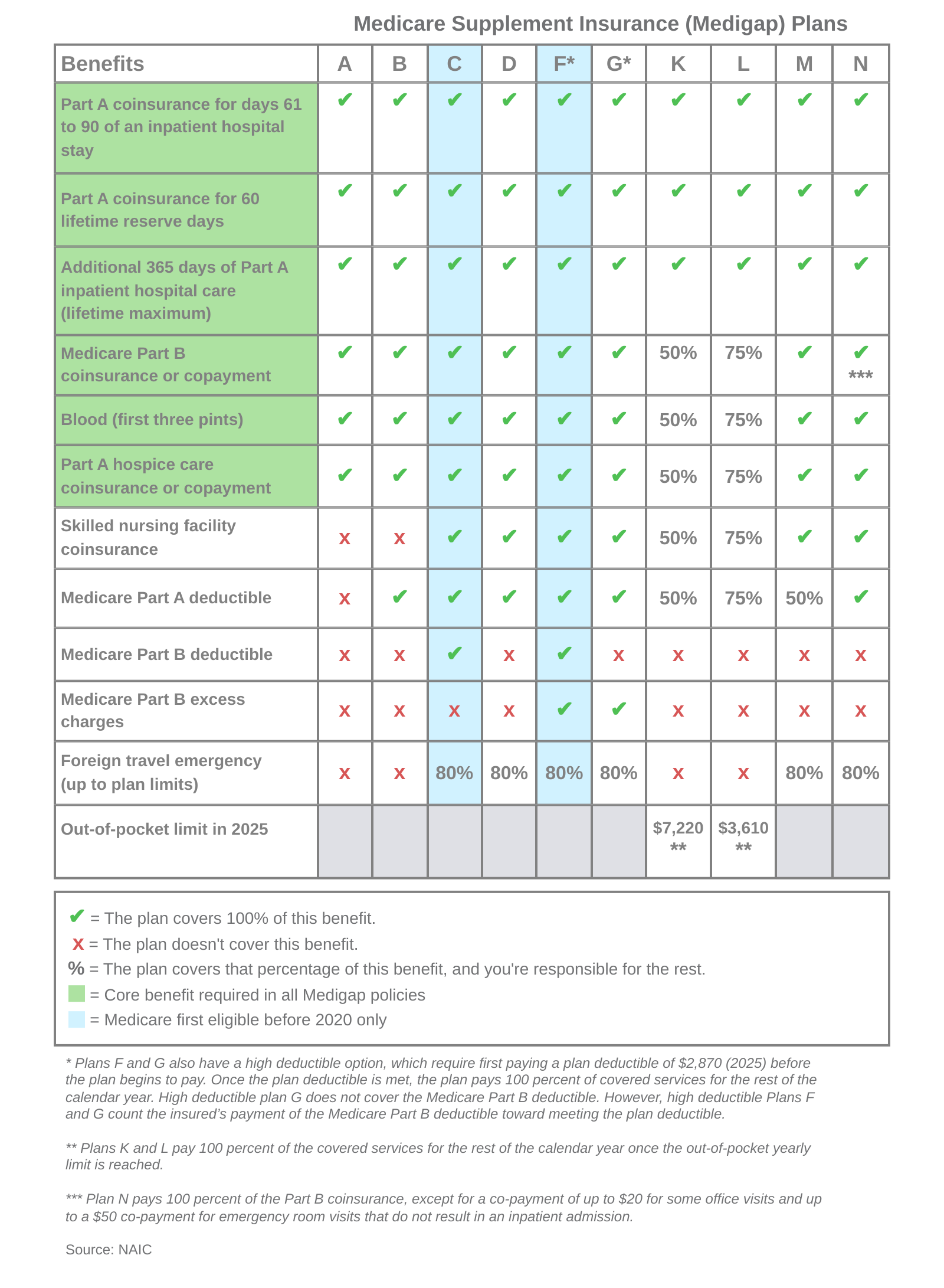

Medicare Supplement (Medigap) plans are designed to help cover the out-of-pocket costs that Original Medicare (Parts A and B) doesn’t cover—like deductibles, copayments, and coinsurance. These plans are standardized across most states, meaning the benefits for each lettered plan (e.g., Plan G, Plan N) are identical regardless of the insurance company, though monthly premiums can vary by provider and location.

Each year, Medicare publishes a helpful resource: the “Choosing a Medigap Policy” booklet, which outlines plan options and updates.

Some insurers offer high-deductible versions of Plan G and Plan F. For these plans, you’re responsible for all Medicare-covered costs (like coinsurance, copayments, and deductibles) until you meet the annual deductible, which is $2,800 in 2025. After that, the plan begins to pay.

Plans K and L have annual out-of-pocket limits that provide added financial protection:

Plan K: Once you reach the $7,060 out-of-pocket limit in 2025 (not including your Part B deductible), the plan pays 100% of covered services for the rest of the calendar year.

Plan L: The 2025 out-of-pocket limit is $3,530, after which the plan also pays 100% of covered services.

Both plans also require you to meet the annual Part B deductible, which is $257 in 2025.

Plan N covers 100% of the Part B coinsurance, except for:

Up to a $20 copayment for some office visits.

Up to a $50 copayment for emergency room visits (waived if you’re admitted as an inpatient).

Medigap plans do not include prescription drug coverage, so if you enroll in a Medigap plan, you’ll also want to consider a stand-alone Medicare Part D plan for medications.

CLICK HERE TO LEARN ABOUT THE MEDIGAP MISTAKE THAT MAY COST YOU LATER!

Yes—Medicare Supplement (Medigap) plans do not use provider networks. As long as your doctor or hospital accepts Original Medicare, they will also accept your Medigap plan. This gives you the freedom to choose any Medicare-approved provider nationwide, with no network restrictions and no referrals required.

Medicare Advantage Plans—also known as Part C of Medicare—are an optional, alternative way to receive your Medicare benefits. These are Medicare-approved managed care plans (such as HMOs and PPOs) offered by private insurance companies that contract with Medicare.

By law, all Medicare Advantage plans must provide at least the same level of coverage as Original Medicare (Parts A and B). Many of these plans go beyond that, offering additional benefits such as prescription drug coverage (Part D), dental, vision, hearing, and even health and wellness programs.

Medicare Advantage plans vary in both cost and coverage depending on where you live. Because they operate on calendar-year contracts, plan benefits, premiums, and networks can change each year—so it’s important to review your options annually to ensure your plan still meets your needs. We help you each year review your options.

Medicare Part D is the part of Medicare that helps cover the cost of prescription drugs. It’s offered through private insurance companies approved by Medicare.

Here’s a breakdown of how it works:

Standalone Prescription Drug Plans (PDPs): These plans provide drug coverage and can be added to Original Medicare (Parts A and B).

Medicare Advantage Plans with Drug Coverage (MA-PD): Many Medicare Advantage plans include drug coverage as part of their all-in-one package.

Covers prescription drugs: Part D helps cover both brand-name and generic drugs that are often not covered by Original Medicare (Parts A and B).

Varied costs: The costs of Part D plans—such as monthly premiums, copayments, and the list of covered drugs (formulary)—can vary between plans and providers.

$2,000 Out-of-Pocket Cap: As of January 1, 2025, the Medicare Part D donut hole has been eliminated, and a $2,000 annual out-of-pocket cap has been introduced. Once you reach this spending limit, your plan will cover 100% of your prescription drug costs for the rest of the year. This is part of the Inflation Reduction Act, which aims to reduce prescription drug costs for Medicare beneficiaries.

Late Enrollment Penalty: If you don’t sign up for Part D when you’re first eligible and don’t have other credible drug coverage, you may face a late enrollment penalty if you decide to enroll later.

Initial Enrollment Period (IEP): When you first become eligible for Medicare (around age 65), you have a 7-month window to sign up for Part D.

Annual Enrollment Period (AEP): From October 15 to December 7 each year, you can join, switch, or drop a Part D plan. Changes take effect on January 1 of the following year.

Special Enrollment Period (SEP): You may qualify for a Special Enrollment Period if you have a qualifying life event (e.g., moving or losing other drug coverage).

We shop your plans, handle paperwork and assist with renewals & policy service for the life of your policy

© 2025 Gregory O’Rourke. All rights reserved.

Protection-first strategies for life, health, and retirement — focused on fixed annuities and insurance solutions designed to protect income, preserve wealth, and provide long-term security.

Independent. No fees for insurance guidance. No pressure. 100% client-focused approach.

Gregory Scot O’Rourke (“Greg”), Licensed Insurance Agent

FL License #G166831 | NPN #21340769 | Multi-State Licensed Agent

Greg is not a registered investment adviser or securities broker-dealer and does not provide investment, tax, or legal advice. This website is for informational purposes only.

Product features and availability may vary by state and carrier. All guarantees are based on the claims-paying ability of the issuing insurer. Coverage is subject to underwriting approval and policy terms. Not affiliated with or endorsed by the U.S. government, Medicare, or the Federal Marketplace.