Most people don’t find out what they’re actually covered for until it’s too late. See your estimated numbers — including what group LTD might actually pay — in under 2 minutes.

Takes about 2 minutes • No contact info required

Select your coverage status and we'll walk you through your real numbers.

We'll calculate your real take-home benefit — including benefit caps, the tax hit, and your elimination period.

Before the numbers — here's why group LTD almost always delivers less than advertised.

When your employer pays the LTD premiums, the IRS treats every benefit dollar as ordinary taxable income — taxed exactly like your paycheck. Your stated benefit is not what lands in your bank account.

Most group plans define disability as "unable to do your own occupation" for only the first 24 months. After that, the definition shifts to "any occupation." If you can perform any job at all — even at a fraction of your former salary — benefits can stop.

What you think you'd receive vs. what actually hits your bank account.

A monthly shortfall feels manageable. Watch what it compounds to.

The amount your plan pays is only half the story. What it won't pay matters just as much.

A condition that develops while on a group plan can make you uninsurable individually the moment that job ends — even if you've never filed a claim.

Your group plan leaves a gap. How long would savings bridge that shortfall?

We'll show you exactly how much income is exposed — and what the numbers look like over time.

Most people believe disability won't happen to them. The numbers say otherwise.

1 in 4 working Americans will experience a disability lasting 90 or more days

What your monthly income looks like if you become disabled today — with nothing in place.

A monthly income loss feels abstract. Watch what it adds up to over the years.

With no coverage, you'd be covering all expenses from savings. How long does that last?

When you quote online with a single carrier, you're guessing. You don't know if that carrier is the right fit for your occupation or health history. We compare top-rated carriers for your specific situation — before you apply to anyone.

Easy to Get Started!

Get a fast quote with our easy-to-fill questionnaire — covering all types of income replacement protection. Just hit the button below to access our secure disability insurance quote platform.

We can even compare options to your current plan and show you exactly where your income gaps are with your existing LTD coverage.

Most carriers show you their number and stop there. We run your profile across top-rated carriers simultaneously and deliver a real comparison — features, premiums, and coverage details all laid out so you can make an actual decision.

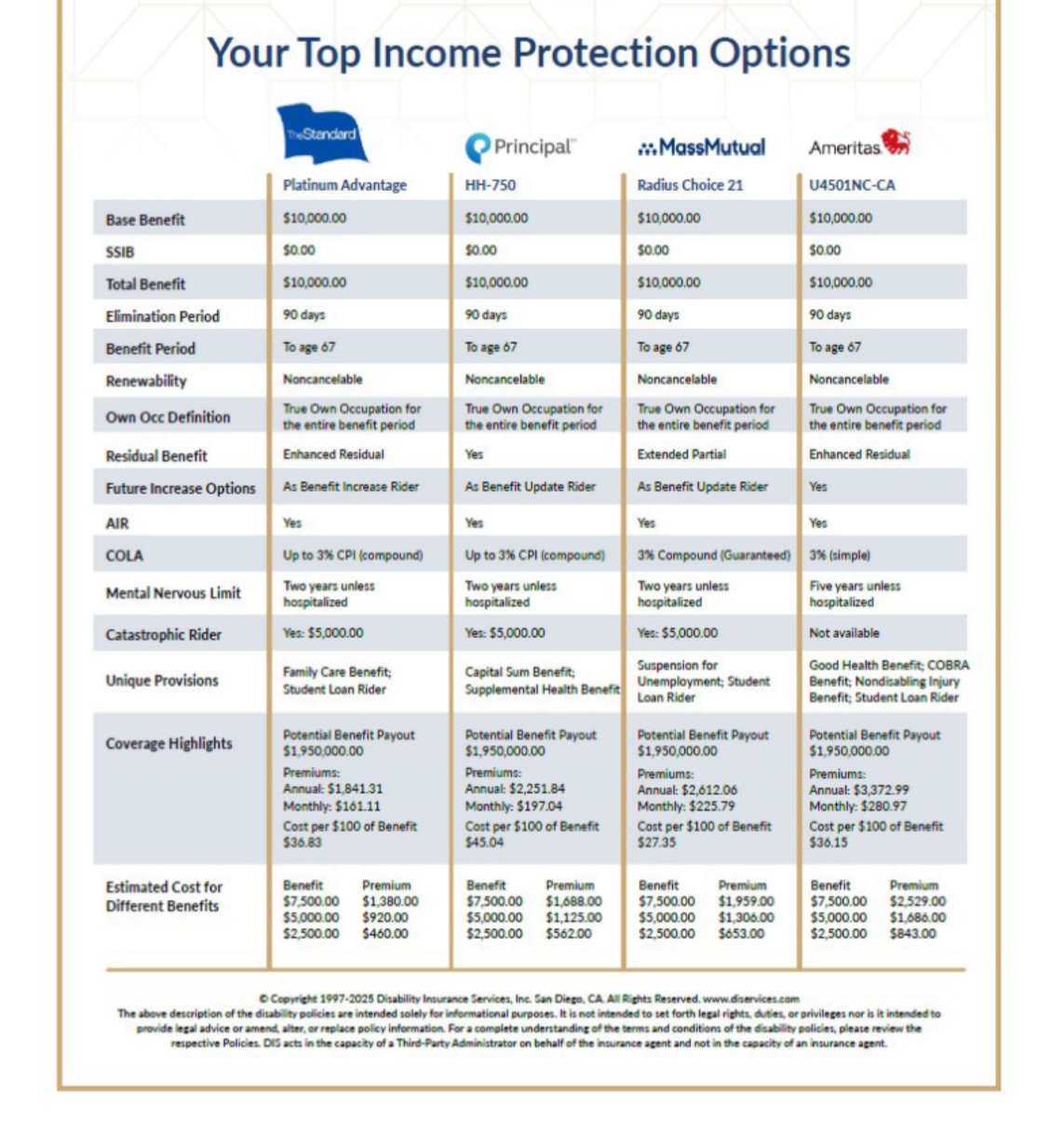

Side-by-side comparison across top-rated carriers — base benefit, elimination period, benefit period, own-occupation definition, riders, and real monthly premiums all in one view. This is what your quote delivers.

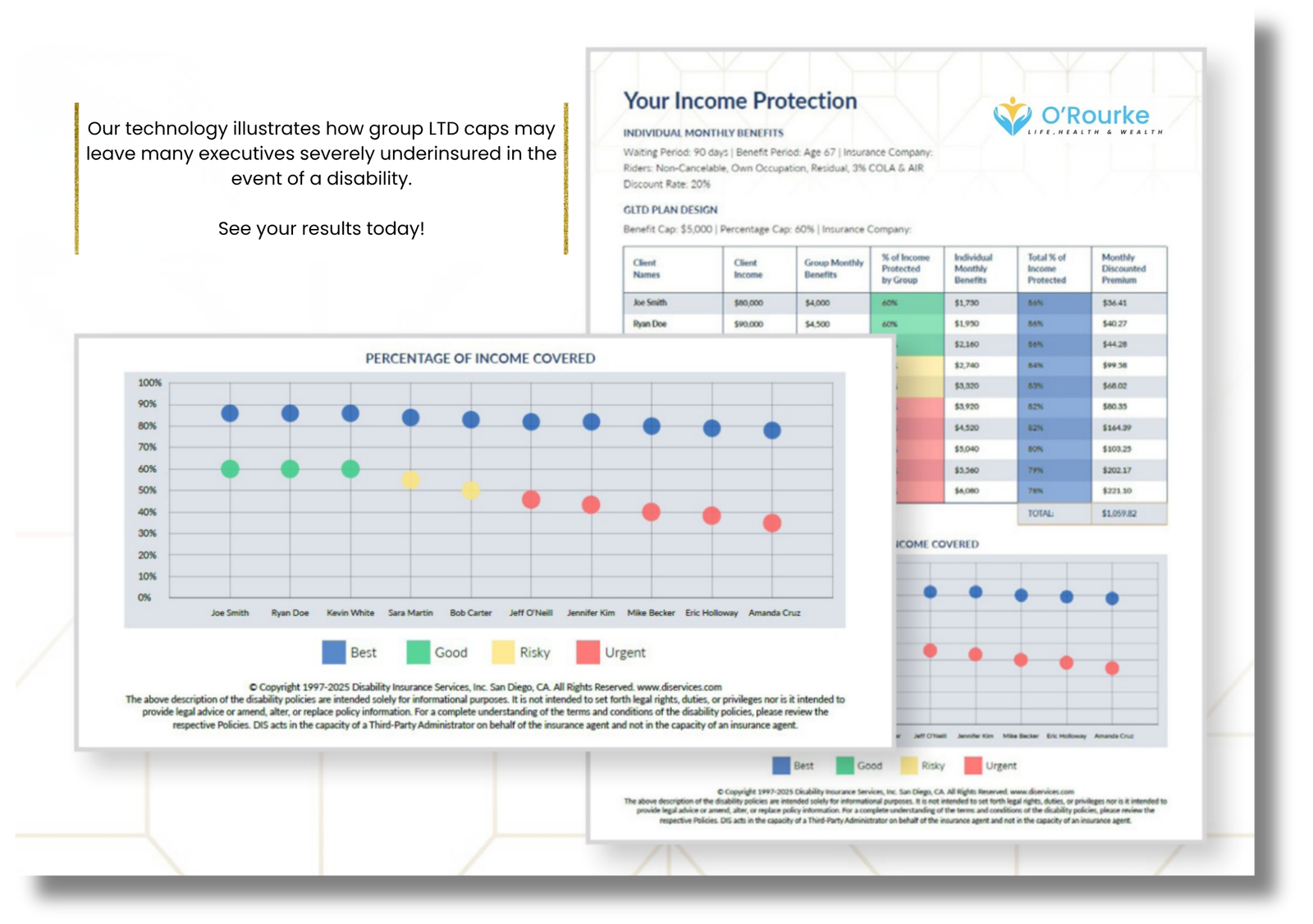

For business owners and employers — our technology shows exactly which employees are Best, Good, Risky, or Urgent based on their current LTD coverage. Branded with your O'Rourke report. Close the gap before it becomes a problem.

Fill out our short questionnaire and we'll run your profile across top-rated carriers — delivering a real comparison built around your occupation, income, and health profile.

As a business owner, a disability creates two crises at once — you lose your personal income and your business expenses keep running. Rent, payroll, utilities, loan payments — they don't stop because you can't work.

Most business owners insure their building, equipment, and vehicles. But when the owner can't work, everything stops — and standard personal DI doesn't cover what keeps the business alive.

Pays your actual business expenses while you're disabled — rent, employee salaries, utilities, insurance, and loan payments. Keeps your business alive while you recover.

If you or a partner becomes disabled, this funds the buyout of that partner's share — so the business continues without a forced sale, legal disputes, or financial strain.

Protects your business from the financial impact of losing a critical employee to disability — covering lost revenue, hiring costs, and the disruption of losing someone irreplaceable.

SBA loans, commercial mortgages, and business lines of credit don't pause if you become disabled. This coverage makes those payments — so a disability doesn't become a default.

Replaces your personal income — draw, salary, or distributions — if you can't work. Own-occupation coverage means you're protected even if you can do other work but not run your business.

A disability rider that continues contributions to your retirement plan while you're unable to work — protecting your long-term financial goals alongside your current income.

When 3 or more employees apply together, everyone gets a rate discount on individual policies. And for qualifying groups, Guaranteed Standard Issue means your whole team can get covered with no medical exams required.

Multi-life discounts — 3+ employees applying together reduces everyone's premium

Guaranteed Standard Issue (GSI) — qualifying groups get coverage with no individual medical underwriting

Employer doesn't have to pay — employees apply together and each owns their own portable policy

Recruit and retain talent — offer a competitive benefit without the cost of a formal group plan

Every business structure is different. Call Greg directly and we'll map out exactly which combination of coverages — BOE, Buy-Sell, Key Person, individual DI — makes sense for your specific situation.

We shop your profile across top-rated carriers simultaneously — finding the best product, best rate, and best fit for your occupation and health profile before you apply to anyone.

Not limited to one company. Not one algorithm. We compare all of them — so you get the best product at the best price for your specific occupation, income, and health profile.

Get My Free Quote →One call shows you every option across top-rated carriers — before you apply to anyone. No pressure, no obligation, no forms that sell your information.

When 3 or more people apply together, everyone gets a significant discount on their individual policy — no formal group plan required. For qualifying groups, no medical exams required for anyone.

📞 Ask Greg About Group Rates