Term vs Whole Life: What's The Difference?

Read our detailed comparison guide

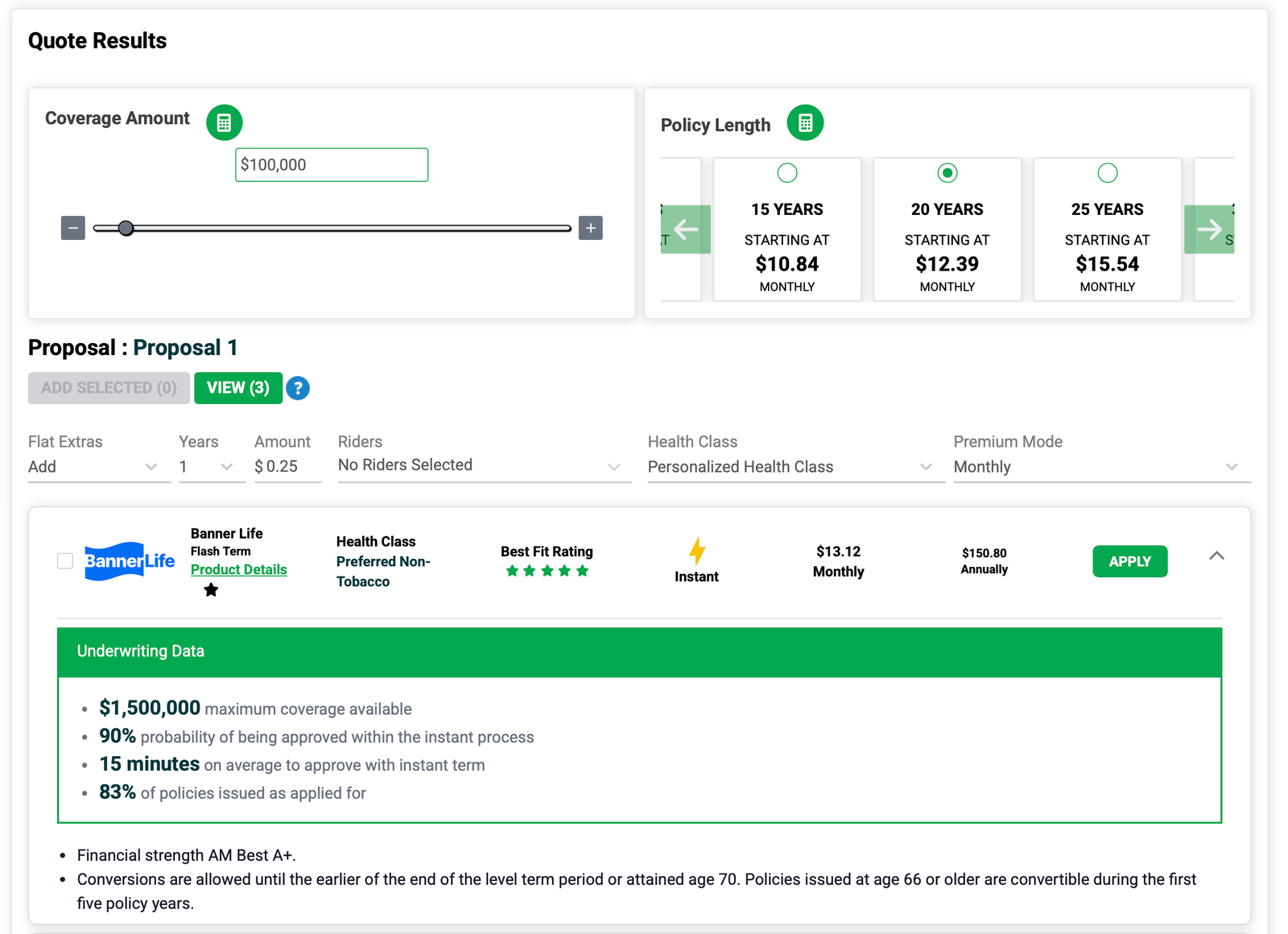

Why price-only shopping fails: most online quote engines show a low number first, then the real underwriting decision comes later. Choose the wrong carrier and you can lose time, pay more, or get an avoidable decline.

A quick quote is an estimate. Your real rate and approval depend on carrier underwriting rules.

Every carrier underwrites differently. What looks "cheap" upfront can change after prescriptions, medical history, build, and carrier guidelines are applied.

The real risk is applying to the wrong carrier first. That can mean delays, higher ratings, or a decline you did not expect. Our goal is to help you avoid wasted time and get the best outcome from the start.

You would not buy a house from one automated estimate alone. You would compare options and get guidance. Life insurance deserves the same approach.

Three advantages most agents and online platforms do not have in the same place: technology, market access, and direct execution. This is how you avoid guessing and get to the best carrier faster.

We do not rely on one carrier, one quote engine, or one guessing game.

Most independent agents have a limited carrier set and manual quoting. Online-only platforms can look slick, but they usually point you to one underwriting decision at a time.

We combine the best of both worlds so you can choose the right path from the start.

No obligation. No pressure. Just clear options and a smarter path to approval.

Why algorithm-only platforms have serious limitations

You've seen the ads: "Get life insurance in 10 minutes! No exam! 100% online!" They're not lying. But here's what they don't say.

Applying to ONE carrier's algorithm without knowing if it's the right fit for your profile

Most "instant online" platforms aren't insurance brokers. They may be tech-enabled front ends for a single insurance carrier.

When you fill out their form, you're applying to ONE specific carrier blindly—without knowing if that carrier is actually best for your health profile, age, or coverage needs.

The result? You might get declined, rated up, or quoted higher than advertised—all because you weren't matched to the right carrier from the start. Then you're back to square one, trying another single-carrier platform.

Same time investment. Dramatically different outcome.

You wouldn't buy a house after seeing only ONE listing. You wouldn't hire the first person who applied for a job. Don't settle for one carrier's algorithm when one call shows you the full marketplace.

See All Your Options FirstOne call eliminates weeks of uncertainty. Just straight answers from a multi-state licensed professional with access to 90+ carriers and data-driven technology.

No forms that sell your information. No lead spam. No algorithm-only decisions. No applying blindly and hoping. No surprises.

Minutes to approval for qualified applicants

450,000+ data points identify your best carriers

Custom laddering strategies save thousands